LawCharge: The most cost efficient attorney-merchant account programs for solo and small firms and the most flexible for mid to large size firms.

Designed by an attorney for attorneys.

LawCharge was the first to bring you merchant accounts designed specifically for attorneys that keep you in compliance with The ABA and your states guidelines for trust accounting. As the pioneers, we are always subject to copy cats but our programs are still the best and hard to beat.

You can accept credit cards with confidence when LawCharge is watching your back.

Virtual Terminal Internet Processing

Virtual Terminal Internet Processing Mobile Processing with Swipe

Mobile Processing with Swipe Process Pin-less Debit Cards

Process Pin-less Debit Cards E-Check and ACH Check

E-Check and ACH Check Traditional Point of Sale Terminal Processing

Traditional Point of Sale Terminal ProcessingLawCharge Recognizes The Inviolability of

Your Trust (IOTA, IOLTA) Account.

We will never debit your trust account. All of our programs comply with the ABA and your state bar requirements regarding accepting credit cards and trust accounting compliance.

Our programs allow you to deposit to both your IOLTA for client funds, and your operating account for fees earned. Any fees will only be debited from your operating account. This avoids any commingling issues as well. Some firms have trust accounts in two or more states but only want fees debited from an operating account in one state.

We can easily accommodate you on this.

Call to Schedule a Demo: 877-977-9740

High Risk Merchant Accounts

If your law firm represents clients conducting what the industry considers high risk business’ you may find a high rejection rate for your own merchant account. LawCharge is able to offer your firm attorney merchant accounts for your high risk clients.

Some examples of high risk businesses would be Bankruptcy/Debt Repair, Collection, CBD/Hemp/Cannabis, Vape Stores, Travel, Fantasy Leagues, and Off Shore merchants.

Because a processor faces a higher rate of chargebacks and fraud in these areas you will either be denied a merchant account or charged higher than average fees. You may also be subject to a ‘rolling reserve’. LawCharge will not gouge you on rates and fees but give you a fair pricing agreement. We will not tie you to a contract period or termination fee.

Adding Surcharges or Convenience Fees

Yes – you can now pass on a portion of your costs when accepting credit cards. As of January 2013 an antitrust lawsuit was settled between merchants and the card networks. You can pass on that portion of your costs, the discount and transaction fees to your client. Typically the discount fee is between 1.65% and 4.00%. This applies to credit and debit cards, but not pin debit cards. The better way to do this is by adding a set convenience fee to the transaction. Your clients must be made aware that you are adding the convenience fee. Please call us to discuss in greater detail.

Currently there are ten states—Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma and Texas—and Puerto Rico that do not permit the passing on of the transaction cost. As lawyers check with your state’s ethics committee even if your state permits the surcharge, your Bar Association may not.

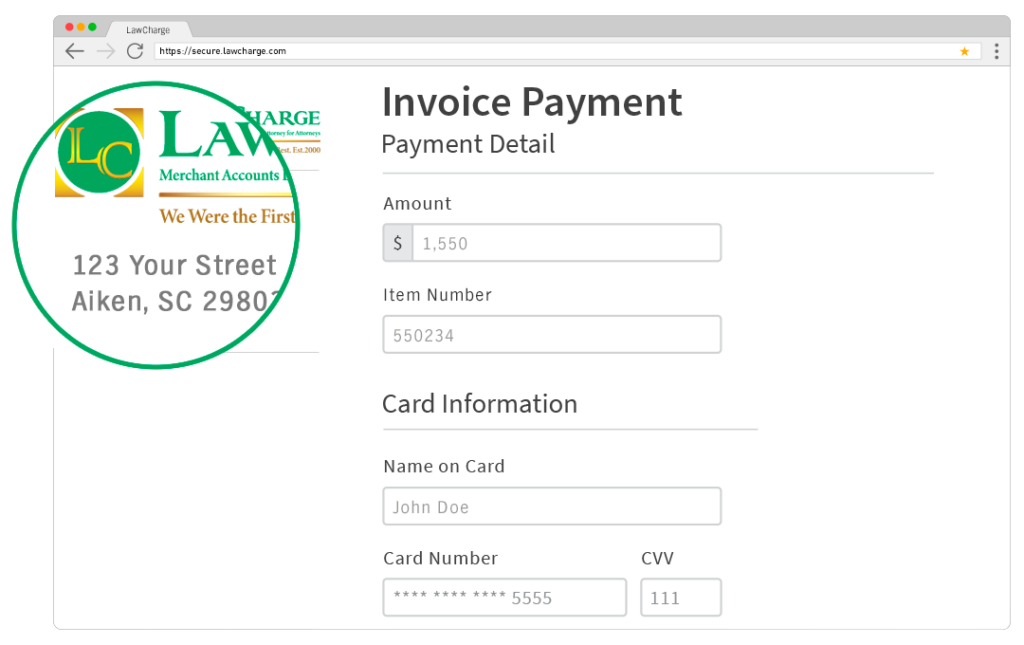

Credit, Debit, E-Check, Invoice Sign and Pay

Discount fees starting as low as 1.69%

-

- Virtual Terminal Internet Processing is one of the most popular and efficient ways for you to accept credit cards. You are able to check on the status of your transactions, easily determine which account (your trust or operating) you want the deposit to be made, review the past 6 months activity, and set up recurring payments.

- Mobile Phone Processing is an easy and convenient way to accept card transactions. You can swipe the transaction with a small device that attaches to your phone or key it in. Our phone programs are the only mobile programs that allow you to properly differentiate deposits between your accounts so you can maintain compliance.

- Private Payment Portal allows the firm to pass the transaction fees on to their client. This option saves the firm some of the processing costs. It also gives you flexibility in your billing as to how you appropriate the transaction costs between the firm and the client. Your client comes to a secured site to enter their card info and amount. The client pays the discount and transaction fees, at the higher ‘capped rate’ of 3.5% and $2.00

- A Point of Sale (POS) terminal is what you find in retail locations. It is best used when the card is present and can be ‘swiped’ to read the magnetic strip or the new EMV chip cards. Most law firms do not have the volume to support the costs of the terminal, the paper, and the ink. These machines are good for high volume activity. Attorneys typically have a fairly low amount of transactions per month.

Some law firms already have POS terminals in which case we can easily re-program them to set up your accounts. Never, ever lease one of these machines. By time your lease is up you would have paid for it three times over.

- Electronic Check Payments: No need to wait for a check to arrive in the mail. Accept checks via ACH and quicken the process. If your client has the cash, you would be saving on the credit card fees.

- E-Sign and Invoicing: Need a document signed? Need an invoice paid? You can do both with our E-Sign with Payments program. Powered by Magensa documents and payments are processed in an all-digital, high security environment.This patented electronic signature software provides forensically identifiable evidence of contractual acceptance with digitized electronic signatures.

Increase your cash flow by 30-40 percent!

Have you ever lost a potential client because they did not have a cash deposit? Do you have slow paying clients? Are there lingering accounts receivable on your books? Do you simply want to bring in more revenue?

Hosted Payment Page and Recurring Payments

With a payment button on your website, LawCharge programs enable your clients to pay you quickly in a secured payment gateway. You, as the merchant, are back dooring into our systems keeping the client information and your business PCI compliant and safe. Set up recurring monthly payments with ease, no more dunning a client for your fees.

Read the First Reviews of LawCharge

The Florida Bar News

July 1, 2001

Proper client intake and credit cards can boost your profitability

By RJon Robins

LOMAS Advisor

Attorney Tracy Griffin, president of Attorney Card Services (now LawCharge 877-977-9740 /www.lawchge@lawchrge.com) observes: “Contrary to what many attorneys think, clients who have not paid their bill do feel uncomfortable communicating with their attorney/creditor. It’s no fun for either the attorney or the client to talk about a case or matter when they both know about, and are trying to politely avoid, the subject of past due bills.”

Tallahassee Branch Auditor Jim Wells, star of the LOMAS video, “Maintaining a TRUSTWORTHY Trust Account,” says there is nothing in Bar rules prohibiting an attorney from accepting credit cards.

… Fortunately, we have a much better alternative now that Ms. Griffin has founded a credit card acceptance program uniquely tailored to the special needs of attorneys,” said Wells.

I have worked with dozens of attorneys to try and find a credit card acceptance company that would credit the entire amount charged to the client’s trust account and deduct the service fee from an attorney’s operating or other account. At the risk of reducing this article to an advertisement piece, I have yet to find even a single other company to offer this unique service.

The Florida Bar News

January 15, 2004

Should your firm be accepting credit cards?

By Jerry Sullenberger

LOMAS Advisor

Selecting the right merchant service provider is extremely important. When you search for merchant services on Google, there are more than 4.4 million hits. So how do you know where to go or who to choose?

A merchant service source you might try is Attorney Credit Card Services, (now LawCharge,lawcharge@lawcharge.com 877-977-9740). ACCS was founded by Tracy Griffin, a Florida attorney, specifically to provide credit card merchant services to attorneys. She has addressed the peculiarities of law firm credit card services. For example, ACCS deposits the full amount of trust transactions into the trust account, and subsequently charges discount rates and service charges for trust credit card activity directly to the operating account, once a month, rather than at the time of each transaction. That certainly simplifies the bookkeeping required. Credit card charges payable into a firm’s operating account are deposited, less the discount rate. She has also eliminated minimum activity fees and has other policies helpful to law firms.